Building data centers currently consumes up to 30 % of the budget—four times more than in 2023.

Overview of Memory Prices in 2026–2027 – Key Findings from SemiAnalysis

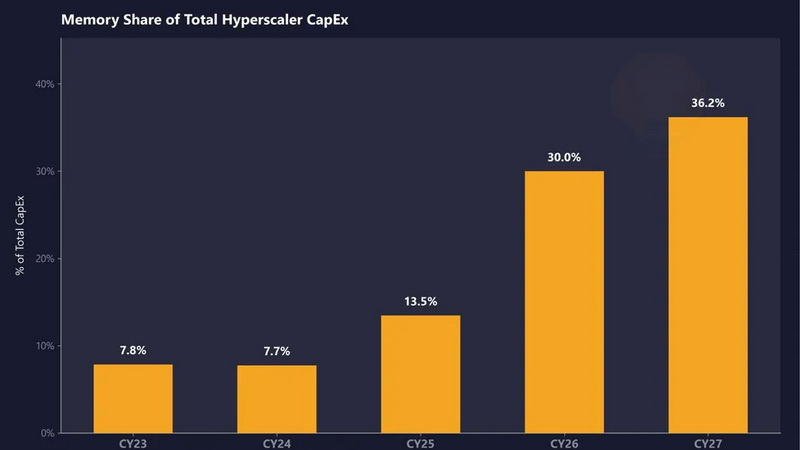

Metric Current Level Forecast (2026–27) Share of Memory in Capital Expenditures of Hyperscalers ~8 % in 2023‑24 ≈30 % in 2026, almost a four‑fold increase over four years

DRAM Prices – more than double by 2026

Average Selling Price (ASP) – two‑digit growth by 2027

LPDDR5 Prices – three‑fold rise from Q1 2025; expected >$10/GB in the current quarter

Key Drivers of Growth

1. Severe HBM memory shortage – AI accelerators continue to face deficits through 2027, driving up server costs.

2. Potential hyperscaler spend – large cloud providers are projected to invest ~US$250 billion in memory, directly impacting equipment prices.

3. Rising component costs – OEM leaders (Dell, Dell‑EMC) note “unprecedented” price increases.

Competitive Differentiation

Company Supplier Preferences Scale of Purchases Vulnerability to Price Increases

Nvidia VVP (Very Very Preferred) DRAM – significantly below market prices Large HBM and LPDDR5 orders Lower vulnerability, ability to influence the market

AMD No such preferences Smaller AI accelerator production Higher sensitivity to memory cost increases

Counterpoint Research Forecasts

- DDR5 RDIMM 64 GB could double in price by the end of 2026 compared with early 2025.

- Nvidia platform servers using LPDDR show the sharpest price spikes due to large memory usage.

Conclusion:

By 2026–27, the share of memory spend in hyperscalers’ capital expenditures will rise to one‑third, and DRAM and LPDDR5 prices will surge sharply. Nvidia maintains an advantage through supplier‑preferred pricing, while AMD faces higher memory costs due to smaller purchasing volumes. This creates significant competition in the AI accelerator market and affects end‑server pricing.

Asted Cloud

Asted Cloud

Comments (0)

Share your thoughts — please be polite and stay on topic.

Log in to comment